| How the State finances housing

Published

Thursday 12th Febuary, 2004

Our national Housing Policy is set out in 'Showing a Trinidad &

Tobago a New Way Home' published in September 2002 by the Ministry of

Housing; this was distributed as a 28-page newspaper supplement.

The document sets out some of the country's serious housing needs and

outlines suggestions for meeting these. The principal challenge

identified is the scarcity of resources to meet the scale of demand; one

estimate suggests that about 14,000 new housing units need to be

constructed every year to meet those needs.

It is important to understand that the State can finance its policies

in 2 principal ways, by spending the money raised from taxes or by

granting tax concessions to particular types of activity and

individuals. In the first case, Government is spending from the pool of

funds we call 'taxpayers' money' and in the second, the grant of the tax

concession has the effect of reducing the size of that pool. Any

realistic estimate of available State resources therefore has to

consider both streams of funding.

State financing of housing exists in 4 parts as follows -

-

Low-income construction via the NHA and the Housing Ministry -

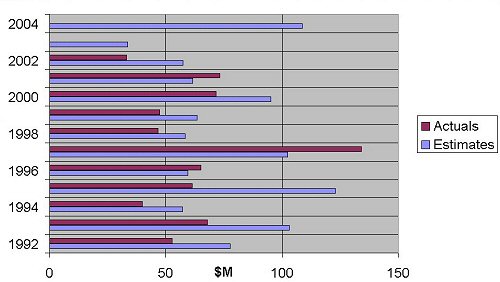

over $715M has been spent by that Ministry in its Capital Program in

the last 10 years. This spending is set out on the attached table.

-

Mortgage interest relief of $18,000 annually to each qualifying

taxpayer in respect of their owner-occupied homes.

-

Tax relief to Approved Mortgage Companies in respect of

mortgages under the official threshold - presently $450,000 in the

East-West corridor.

-

Tax relief to property developers in respect of profits on units

built for sale under that threshold.

This basket of measures is not in fact outlined in the Housing Policy

and it is unclear, after enquiries with the relevant Ministries, whether

there is any overview as to the quantities of money deployed via these

policies. Given the importance of housing to achievement of developed

nation status, it is disappointing that we were unable to obtain

reliable figures for the number of homes built for this immense

investment via the Ministry. Without such elementary data we are unable

to assess the unit costs or effectiveness of various design and

procurement approaches.

It is a given that policies ought to be subject to periodic review so

as to assess their effectiveness in satisfying the original goals and

indeed whether those goals themselves need to be adjusted. The Housing

policy does acknowledge that "…a major deficiency in the Housing and

Settlements sector is in policy making and coordination of strategic

planning and programming…" It is clear that steps are being taken to

address this critical matter.

The details of the Housing Ministry's capital spending show a

consistent pattern of large variances between the estimated expenditure

and the actual, with the norm being that less money is spent than

budgeted. The point being that annual shortfalls in budgeted expenditure

imply a deepening of the level of unmet housing needs. There is a need

for research into the reasons for the variances since this can help in

selecting the most effective procurement measures and designs for this

sector.

If we are unable to say with certainty what is the level of funds

committed via these policies, it is impossible to evaluate their

effectiveness.

Some basic points can be made -

Value for money - As I said in the last installment,

the quality aspect of housing is arguably more important than the more

obvious issue of quantity. We would need to enquire whether the funds

spent in providing proper infrastructure and title to 'established'

squatter communities is better value for money than building new homes.

Mortgage Interest relief - This is a universal benefit

that all qualified people are entitled to claim the $18,000 relief,

regardless of the level of income. All claimants, from the wealthy to

the more modest salaried homeowner, therefore enjoy this. The benefit

would have far greater impact on the latter and conversely, its loss or

reduction would have little real effect on the wealthier claimants. One

could even say that the standard of living enjoyed by the middle class

(for the sake of this discussion, let us say those living in houses

worth less than $500K) is significantly higher today that that which

prevailed 20/25 years ago.

Delivery Capacity - When we examine the table showing

the Housing Ministry's Capital Program, we can see that there is

expected to be a dramatic increase in expenditure from just over $33M

last year to almost $109M this year. Given the stated deficiency at the

Housing Ministry in strategic planning and programming as well as the

consistent underspend, it is indeed cause for concern that spending is

being more than tripled in just one year.

Policy overview - In the course of doing the research

for this column, it is clear that there is a sense of urgency in

augmenting the research capacity of the relevant Ministries.

In economists' terms, without the necessary overview the State could

be making a potent misallocation of funds in terms of the consequences -

poor living conditions, environmental degradation and so forth.

|